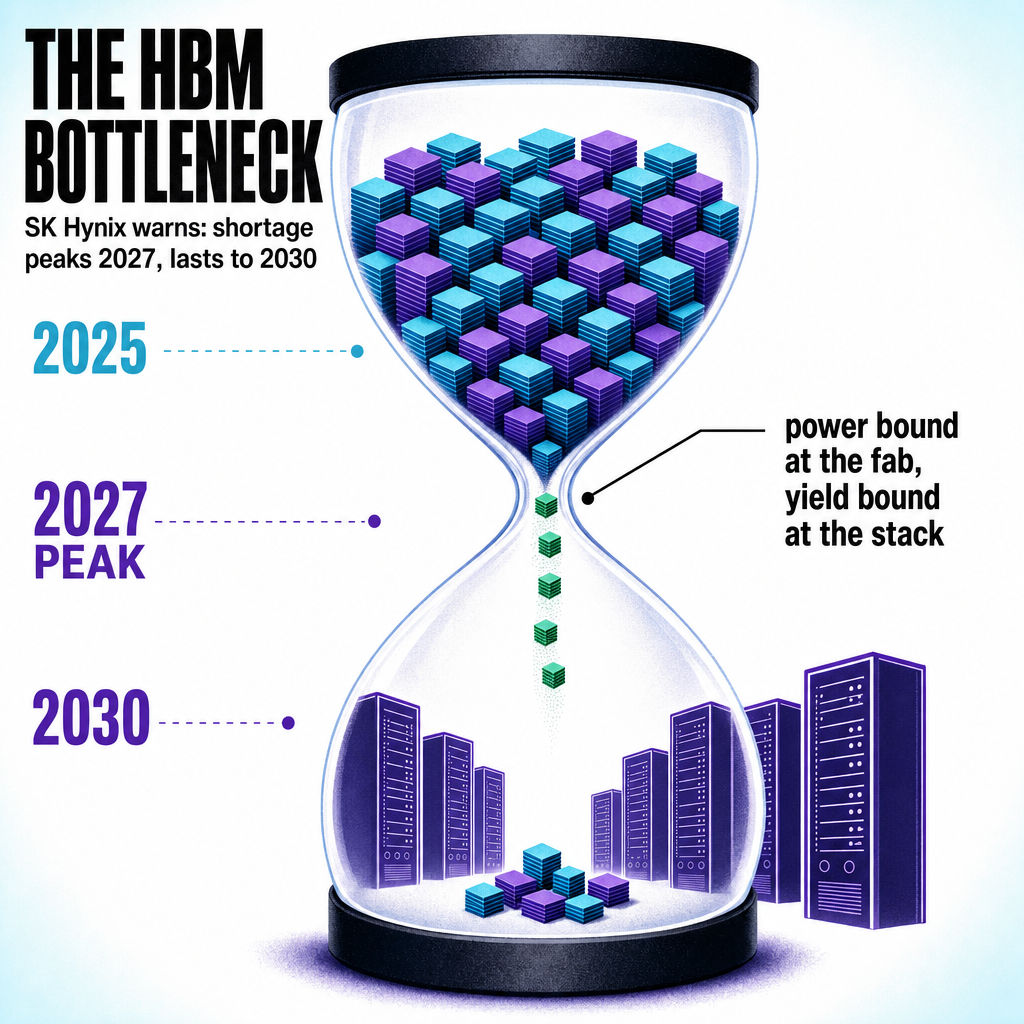

SK Hynix, the world's second-largest memory maker, warned the AI memory shortage will peak i...

SK Hynix, the world's second largest memory maker, used its Nasdaq listing day to deliver a message the AI industry has been reluctant to hear. The company warned that the shortage of high bandwidth memory, the specialized DRAM feeding every serious AI accelerator, will peak in 2027 and stretch into 2030. If you are building on top of hosted inference APIs, this is the supply chain reality sitting underneath your roadmap.

HBM is the stacked DRAM that sits next to the compute die on an H100, a B200, or an MI300. Unlike commodity server memory, it is power bound at the fab and yield bound at the stack, meaning you cannot simply build another line and have chips flowing in a quarter. The process of bonding multiple DRAM dies vertically with through silicon vias is delicate, and every generation (HBM3, HBM3e, and the incoming HBM4) tightens tolerances further. SK Hynix telling the market that the shortfall gets worse before it gets better is not marketing. It is a supplier managing customer expectations three years out.

For teams shipping generative AI in production, three things follow. First, token prices stop trending down. The dramatic collapse in cost per token from 2024 through 2026 was riding a wave of oversupplied inference capacity and aggressive pricing from clouds trying to win workloads. That tailwind is ending, and pricing power shifts back to whoever holds the accelerators. Second, capacity becomes the real rollout risk, not model choice. Your Bedrock, Azure, or Vertex quota is downstream of somebody's HBM allocation from Samsung, Micron, or SK Hynix, and when that allocation tightens, quotas tighten with it regardless of your contract tier. Third, smaller fine tuned models running on prem or on device stop being a philosophical preference and start being a hedge against your primary provider throttling you. The same goes for aggressive KV cache reuse, quantization down to 4 bit or lower, and routing cheap traffic to open weight models like Llama or Qwen.

The frontier lab race is a hardware race dressed up as a software race, and the teams that survive the next 24 months will be the ones whose serving stack was designed for a memory constrained world rather than an abundant one. Watch for two signals over the next year. Watch whether hyperscalers begin quietly rationing frontier model access to enterprise customers, and watch whether the major labs start publishing efficiency benchmarks as loudly as they publish capability benchmarks. Both will tell you that the industry has finally accepted what SK Hynix said out loud today.

Originally posted on LinkedIn.