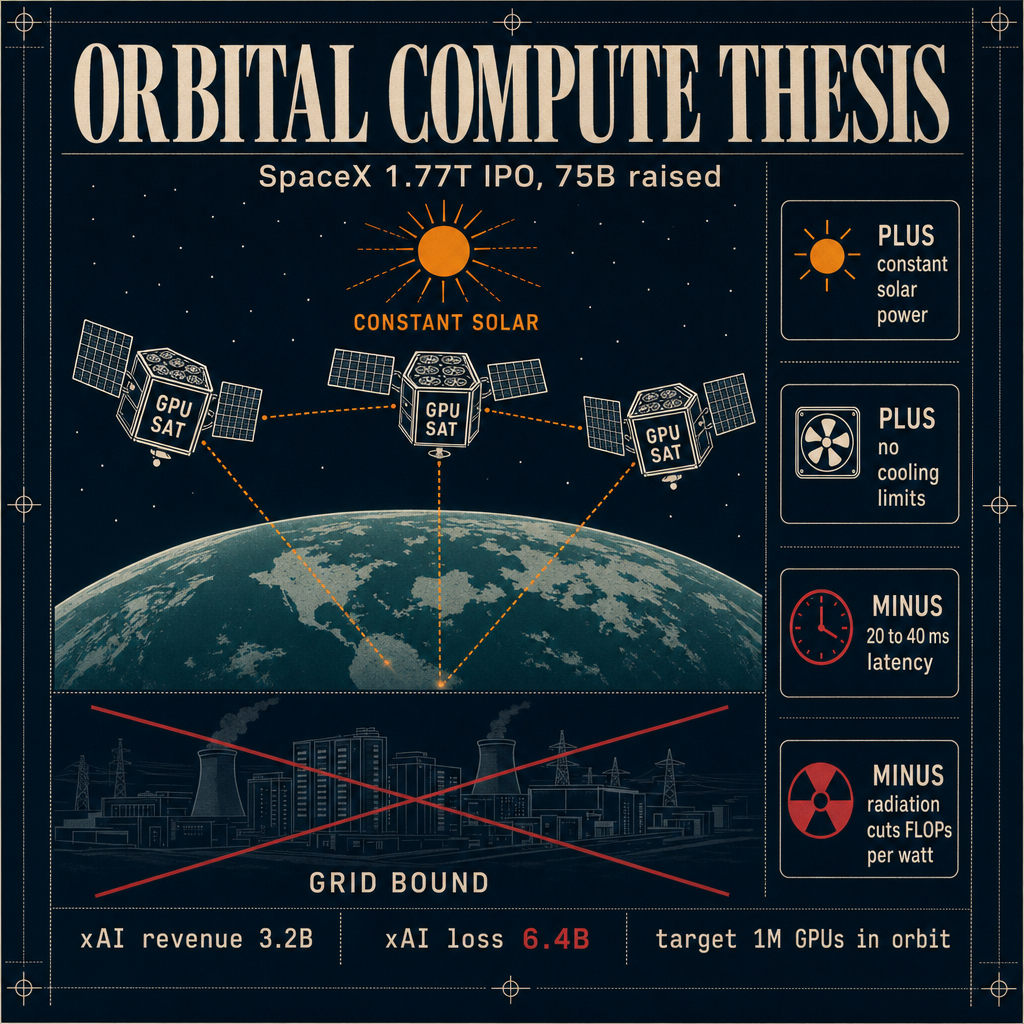

SpaceX went public at a $1.77 trillion valuation, raising about $75 billion, and the prospec...

SpaceX went public this week at a 1.77 trillion dollar valuation, raising roughly 75 billion dollars in what is now the largest IPO on record. What makes it interesting for anyone tracking AI is that the prospectus reads less like a launch company filing and more like an AI infrastructure thesis, with orbital data centers positioned as the long term play.

The setup goes back to February, when Musk merged xAI into SpaceX. The S-1 sketches out a constellation of up to a million GPU packed satellites running both training and inference in orbit, where solar energy is constant and the terrestrial constraints of power delivery and cooling largely disappear. The financials underneath give the strategy its urgency. xAI lost 6.4 billion dollars on 3.2 billion in revenue, and the IPO is effectively the funding vehicle for the compute thesis. Without a public market raise of this size, the orbital roadmap simply does not pencil out.

The reason this matters technically is that every frontier lab is now power bound rather than chip bound. Anthropic, OpenAI, and Google are all negotiating gigawatt scale deals directly with utilities, and grid interconnect queues in the US now stretch past five years in some regions. Orbital compute sidesteps the grid entirely, which is the whole point. The tradeoffs are brutal though. Latency from low earth orbit adds 20 to 40 milliseconds round trip, radiation hardening cuts effective FLOPs per watt by a meaningful margin, and inter satellite laser links cap aggregate bandwidth well below what you get inside a terrestrial data center fabric. None of these are solved problems, and some of them may not be solvable at the scale Musk is describing.

For builders this is not a 2027 concern, and probably not even a 2030 concern in any production sense. But it does tell you where inference cost curves are heading and how the largest players are thinking about the next decade of capex. If orbital training works even partially, the cost per token floor drops again, and on premise GPU economics get harder to justify for anything except low latency or regulated workloads.

What I will be watching over the next year is whether the first demonstrator satellites actually fly and whether the FLOPs per watt numbers in orbit come anywhere near the marketing. The honest read is that the IPO is partly a bet that compute will become a utility delivered from space, and partly a bet that public markets will fund a decade of losses to get there. Both bets need to land for the thesis to hold, and the second one may turn out to be the harder of the two.