OpenRouter just raised $113M at a $1.3B valuation, and its business model is almost deceptiv...

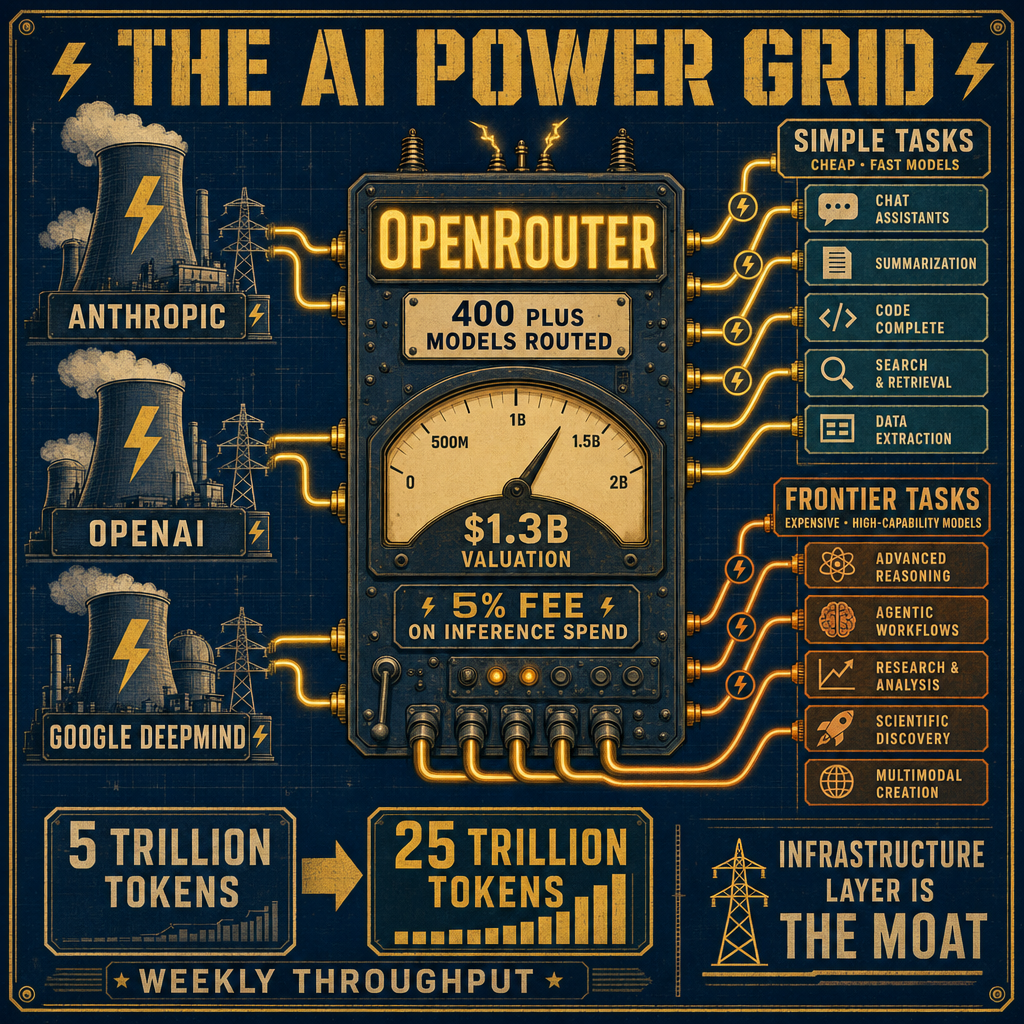

OpenRouter, a company most people outside AI engineering circles have never heard of, just raised 113 million dollars at a 1.3 billion dollar valuation. The reason matters more than the headline number: the firm makes its money not by training models but by routing requests between them, and that quiet middle layer is turning into one of the most valuable real estate plots in AI infrastructure.

The business model is almost deceptively simple. OpenRouter sits between you and over 400 AI models, routes your request to the right one, and takes roughly 5 percent of the inference spend that passes through. No frontier training runs. No proprietary model. Just routing. For a company avoiding the billion dollar capex arms race that defines the rest of the industry, that is a remarkably clean position.

The scale tells the real story. Weekly token throughput grew from 5 trillion to 25 trillion tokens in a short window, a five times jump. What that number actually reveals is a behavioral shift among the people building with AI. Enterprises and developers are not betting on a single model anymore. They are running workloads across many models at once and need someone to manage the traffic, handle failover when a provider goes down, and normalize the API differences between vendors.

A useful way to think about it is a wholesale electricity broker. The power plants, Anthropic, OpenAI, Google DeepMind, generate the energy. OpenRouter makes sure it reaches you efficiently and cheaply, and clips a small fee on the way through. The broker does not need to own a turbine to matter.

Technically, this matters because multi model architectures are becoming the default pattern. You route cheap, fast models to simple classification or extraction tasks, and reserve expensive frontier models for the cases where output quality actually justifies the cost. Doing that by hand across providers is painful. OpenRouter is the plumbing that makes it tractable at scale, and the 5 percent take rate is what developers are willing to pay to avoid building it themselves.

The deeper signal is that the AI infrastructure layer is quietly becoming as valuable as the models themselves. We saw this pattern in cloud computing, where load balancers, CDNs, and observability companies built enormous businesses sitting next to the hyperscalers. The open question worth watching is whether routing remains a durable moat once the big labs ship their own switching tools, or whether neutrality itself is the moat. A broker who works for you, not for any single model provider, may be exactly what a fragmented model landscape requires.

Originally posted on LinkedIn.